Welcome to the Producers Portal!

Learn More About Credit Insurance

Credit Insurance Overview

What Is Credit Insurance?

Business credit insurance covers a company’s accounts receivable, which typically represent more than 40% of a company’s assets. This protection insures against unexpected bad debt losses outside of the insured’s control due to commercial and./or political risks, such as insolvencies, protracted default, repudiation, acts of war and government regulation or restrictions.

Commercial Risk

- Insolvency – Includes court protection such as Chapter 11 in the U.S. or Companies’ Creditors Arrangement Act in Canada

- Protracted Default – Unpaid invoices 90 days past due date

- Repudiation – Refusal to take up goods shipped and delivered as per contract

Political Risk

- Inconvertibility

- Contract frustration as a result of government action

- Public Buyer Default

- Act of war (other than wars between the five super powers: China, France, Great Britain, Russia and the U-S.)

- Government regulation or restrictions

Why Insure Accounts Receivable?

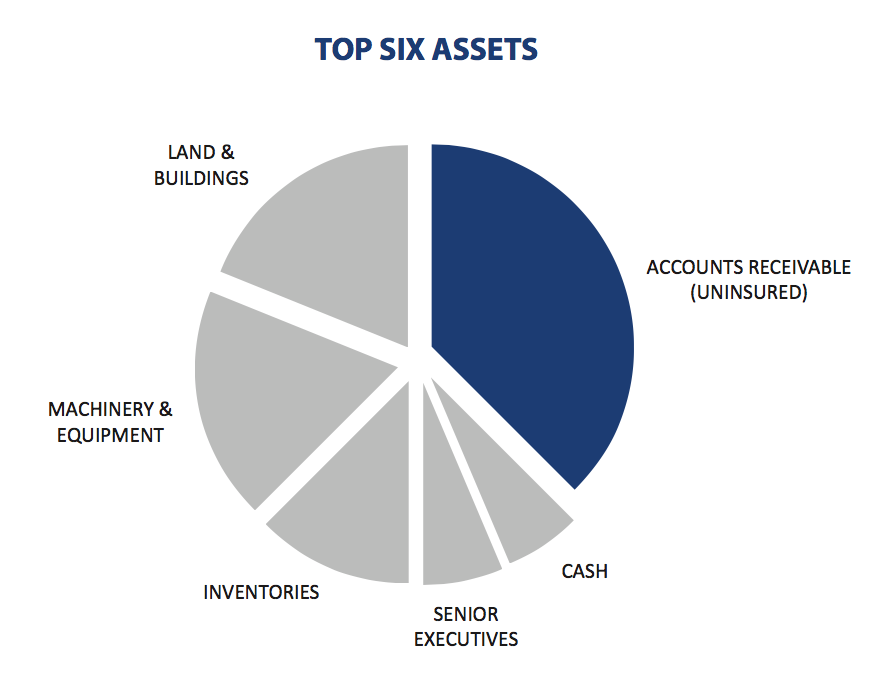

Accounts receivable are often a company’s only uninsured asset, yet they are one of the most vulnerable to loss and are more likely to be affected by business cycles.They provide the cash flow – the lifeblood – for a business and usually represent the highest cost to maintain (funded through bank borrowings and cost of delinquencies).

How Credit Insurance Benefits Your Clients

How credit insurance benefits your clients:

Credit insurance is a partnership with financial risk management.

- It puts a ceiling on exposure to losses.

- It complements sound financial risk management.

- It assists a company in safely developing new markets.

- It frees time to focus on other important aspects of the business.

Most companies are exposed to credit risk.

- Few companies can compete without extending credit.

- Being an unsecured creditor exposes companies to risk

- Trade credit is usually two to three times larger than bank overdraft lending.

- Risk is much higher than bank lending, yet trade credit is not secured or insured

- Accounts receivable are one of the largest assets under the control of the chief financial officer, yet few safeguards are in place.

- Like any other investment, accounts receivable requires safeguards.

- Sound credit management practices

- Credit insurance

- Two main risks to the investment are:

- Profit erosion through interest expense on late payments

- Bad debt losses from clients unable to pay

Credit insurance provides companies with added security

Overall bottom line benefits

- Insuring accounts receivable results in several bottom-line advantages for your clients.

- They can reduce credit risk and improve financial planning, gaining more confidence that financial objectives will be met and cash flow projections will be secure – see Quantifiable Benefit #1

- They can enhance financing by borrowing more against their receivables – see Quantifiable Benefits #2 and #3

- They can safely expand sales, both domestically and abroad – see Quantifiable Benefit #4

- They gain an important complement to their credit management practices.

1. Reduce Credit Risk and Improve Financial Planning

A. STRENGTHEN THE BALANCE SHEET AND AVOID THE UNEXPECTED

- Protect one of the company’s largest assets – accounts receivable.

- Safeguard sales and gross margin -‘the lower the gross margin percentage, the more sales and production required to replace a bad debt’- see Quantifiable Benefit #1

- Avoid unexpected demise of a large customer than can put the company out of business – ensure all your eggs are not in one basket.

- Ask – What amount of loss would seriously hurt this company’s financial stability or yearly profit? How many accounts are over that amount?

- Ask- what percentage of total or current assets does your customer’s accounts receivable represent?

- Ask- How does this amount relate to the Company’s equity?

B. SECURE THE COMPANY’S CASH FLOW

- Reduce impact bad debt can have on cash flow.

- Protect the company’s most liquid asset next to cash – accounts receivable.

- Smooth the bumps in cash flow caused by protracted default.

- Avoid domino effect – a large proportion of business failures are directly attributed to uncollectible accounts.

C. FORECAST BAD DEBTS MORE ACCURATELY

- Reduce bad debt reserves to improve current year’s profitability.

- Free up capital to more productively invest elsewhere. Put a ceiling on bad debts/credit risk.

- Ask – Do you conservatively reserve or over-reserve for bad debts?

- Ask – Have you made any special situation reserves over the past five years?

- Ask – Would it be reasonable to assume another expected situation could occur over the next five years?

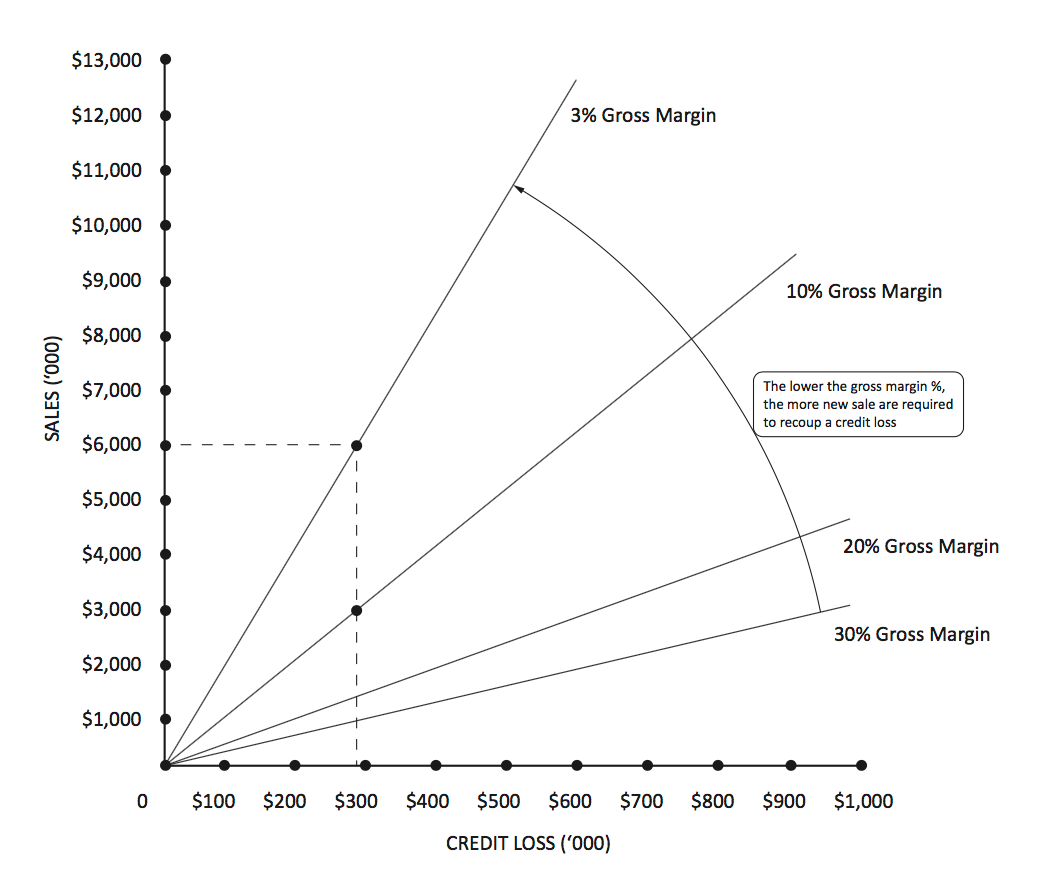

Quantifiable benefit #1

New Sales Necessary to Replace a Credit Loss

Example: If your customer sells on a 10% gross margin, the loss of a $300,000 risk will require $3 million in new sales to replace it. If your customer has a 5% gross margin, the company must generate $6 million in new sales.

2. Enhance Financing

A. IMPROVE ACCOUNTS RECEIVABLE MARGINING

- Many companies can increase margining to as high as 85% on domestic accounts receivable to improve the company’s liquidity.

- Foreign accounts receivable are often not recognized by banks, and companies receive no margining. Again, with credit insurance, this can be improved to as much as 85%.

- See Quantifiable Benefit #2 for a graphical presentation of this benefit and a worksheet to determine if this will be of benefit to your customer.

- Look for companies growing – especially growing abroad – and determine their current bank margining requirements.

B. REDUCE THE COST OF BORROWING

- Many banks reduce the operating line of interest rate by 1/ 4% – 1/2% when companies enhance their accounts receivable with credit insurance.

- This can significantly reduce the net cost of credit insurance to your customer.

- See Quantifiable Benefit #3 or a graphical presentation of this benefit and a worksheet to determine if this will be of benefit to your customer.

- Look for companies borrowing at rates of prime plus 1/2% and higher that have large operating lines that are substantially used.

C. REDUCE BANK SECURITY REQUIREMENTS

- Enhance the bank’s security package by assigning the policy to the bank. Many banks will in turn reduce personal and other security requirements.

- Smaller companies that usually provide proportionally more security (and personal security) to banks can benefit most.

- Ask your clients if they provide personal covenants to their bank or if they feel they are substantially over-secured at their bank.

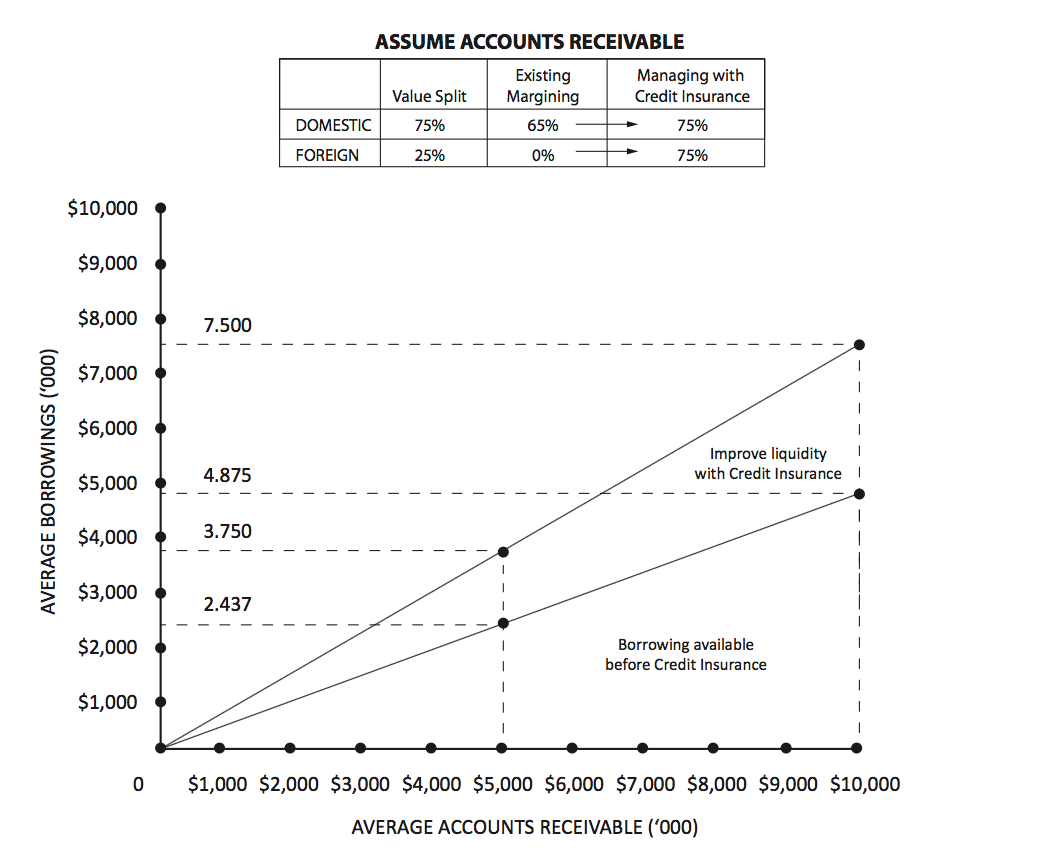

Quantifiable benefit #2

Improve Borrowing and Liquidity

Example: In this scenario, a company that has on average $5,000,000 in accounts receivable, and is borrowing from the bank against accounts receivable, will increase available borrowings 54% from $2,437, 500 to $3,750,000. A company with $10,000,000 in accounts receivable will improve borrowing from $4,875,000 to $7,500,000.

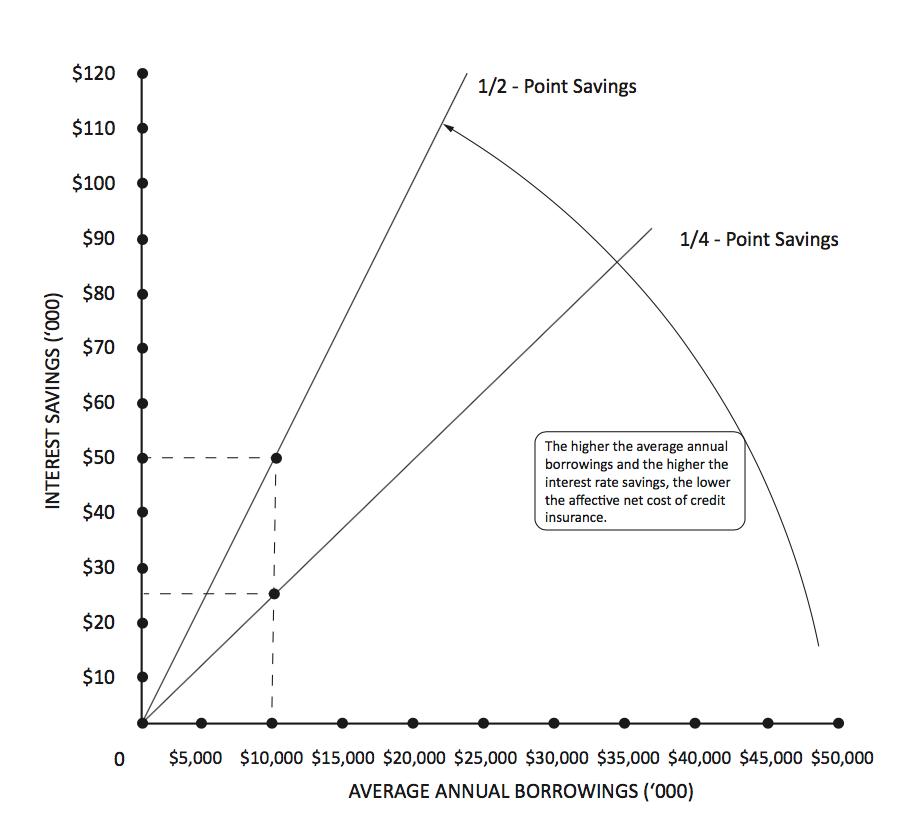

Quantifiable benefit #3

Reduce Borrowing Costs

Example: If a customer/prospect borrowed on average $10,000,000 at an interest rate of prime plus 1% and credit insurance could reduce the interest rate by 0.25% (because the bank felt cash flow and accounts receivable were better protected) , the company would reduce annual interest costs by $25,000. If the estimated net cost of credit insurance, after routine bad debts, translated to $60,000, the effective net cost of credit insurance, after interest savings, would be only $35,000.

If a 1/2% rate reduction could be achieved, the savings would total $50,000 and the effective net cost of credit insurance would only be $10,000.

3. Expand Sales

The global market is very competitive. And there are many additional business risks and complications inherent in selling abroad. Most strong management teams will want to minimize those risks in their control. Credit risk is in their control when credit insurance is in place.

Credit insurance is a tool that can help a company increase sales of nominal risk. The higher a company’s gross margin percentage, the greater the contribution from these incremental sales. This incremental revenue/profit contribution effectively reduces the cost of credit insurance to your client.

See Quantifiable Benefit #4 for a graphical presentation of this benefit and a worksheet to determine if this will be of benefit to your client.

A. EXPAND SALES TO NEW AND HIGHER-RISK CUSTOMERS AND NEW MARKETS TO WHICH SALES MAY BE CURRENTLY RESTRICTED

- Leverage the underwriter’s extensive proprietary information database and an insurance pool underwriters will often go on risk with companies that your customer perceives to be an abnormally high risk because of proprietary information obtained from buyer visits.

- Ask

- Are there any higher-risk customers or markets to which you are restricting sales?

- Who are they? Credit Insurance may allow you to increase your credit limit.

B. SELL ABROAD ON MORE LENIENT PAYMENT TERMS IMPROVING THE EXPORT SALES EFFORT

- This can also eliminate the cost and hassle of doing business on letters of credit

- Tap into the extensive international database and knowledge the underwriters developed through writing risk on over 160 countries around the world.

- Ask

- Could selling on open credit improve your sales effort by putting you in a more attractive competitive position?

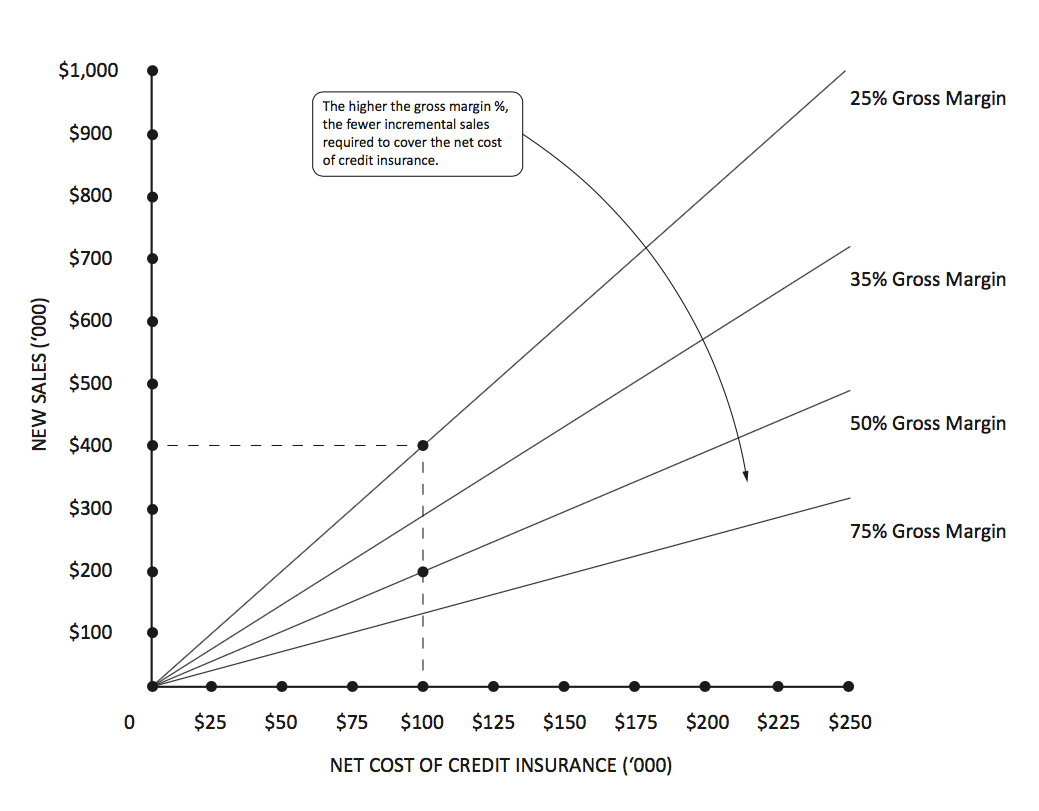

Quantifiable benefit #4

Incremental Sales to Pay For Credit Insurance

Example: If your customer sells on a 25% gross margin, and the cost of credit insurance, after routine bad debts are netted out, is $100,000, only $400,000 in new incremental sales are required to pay for the credit insurance. If your customers’ gross margin percentage is 50%, only $200,000 in incremental sales are required.

4. Complement Credit Management

Credit insurance works in partnership with your client’s credit management staff. We often are in daily or weekly contact with the credit manager. Credit insurance is a tool to assist the credit manager and by no means can be a substitute for a good credit manager and strong credit controls.

Most of these benefits are not quantifiable and are related to credit management. It is important that the credit manager is an ally in the sale. His or her support, or lack of support, usually weighs heavily on the decision maker. Credit insurance must be positioned so the credit manager does not see it as a threat, but rather as a tool for his or her personal benefit as well as the company’s benefit.

A lot of the benefits explained in this section will help to ensure that the credit manager will not be a barrier to the sale. If the credit manager sees credit insurance as a tool that helps him or her to do a better job and eliminates personal risk associated with the demise of a large risk, he or she may even champion credit insurance. If this happens, the cost of credit insurance should become less of an issue.

A. A PARTNERSHIP WITH CREDIT MANAGEMENT

- The credit manager maintains absolute control of the majority of limits, acting on all requests for credit below a discretionary limit if one is set on the policy.

- For larger amounts above this discretionary limit, our underwriters work with the credit manager to determine the creditworthiness of the buyer.

- The underwriter provides the endorsement on these larger buyers, the demise of which can hurt your customer, so the credit manager can release shipments with confidence.

- The underwriter provides a second opinion to the credit manager and help deflect sales force pressures.

- In very high-risk situations, we work closely with the company’s credit management and Underwriter to reduce exposures to these excessive risk situations.

B. ACCESS TO PROFESSIONAL CREDIT MANAGEMENT, PERSONNEL AND SYSTEMS

- Our underwriters have the authority to personally analyze and approve large limits.

- Highly skilled underwriters and analysts know the customer’s industry and major buyers.

- Periodic monitoring of approved limits.

C. FOCUS SALES EFFORTS

- The underwriter’s focus on higher risk buyers provides information to your clients, so they can focus their sales efforts and build their business on strength as opposed to weakness.

D. FREE UP CREDIT MANAGEMENT TIME

- Credit insurance policies require minimal administration and frees up some of the busy credit officers time to focus on his or her many other activities.

- Credit Insurance also reduces information collection and analysis costs associated with these larger clients.

5. Other Benefits

- Obtain large risk capacity on buyers that can only be provided by a credit insurer with strong reinsurance arrangements.

- Protect against unforeseen foreign political events that could negatively affect sales.

- Cover your work-in-process to protect against the insolvency of a customer for which you are in the process of producing customized goods to a specific order.